- January 18, 2023

October 18, 2022

At its core, the work of Nathan Associates has always been about advancing the United States’ role in advocating for a safer, more equitable, and resilient global future.

From helping rebuild Europe after the devastations of the Second World War to conducting major economic development projects in over 120 countries today, Nathan Associates’ hallmark resides in its cutting-edge ability to deliver innovative, tailored, and forward-looking solutions in service of a better tomorrow.

It feels both exciting and unsurprising, as Nathan Associates celebrates 75 years in business, to be discovering new ways to apply that global perspective and experience. If we hadn’t already known, the last few years would have taught us that the world is more interconnected than ever, and at Nathan Associates we believe that our unique brand of insight and technical analysis is essential to tackling today’s local, national, and regional challenges.

Why Federal Services? And Why Now?

Rapidly-shifting geopolitical realities—whether it’s the COVID-19 health crisis, the growing economic instability, or the invasion of Ukraine—are cross-cutting issues with intense repercussions internationally as well as at home. We therefore asked ourselves: how can we continue to help clients be ahead of the curve in preempting future risks and creating the most resilient and scalable solutions? How can we leverage our perspective, expertise, and global experience to address clients’ needs?

This was the reasoning behind the decision to establish a new structure dedicated to supporting U.S. Federal Agencies in achieving their priorities.

“From our vantage point, it’s a natural extension of the work we’ve been doing for decades. No matter the sector—whether it’s economics, gender, climate, diplomacy, or national defense—no other firm can draw on the kind of history and knowledge we can bring or offer the 360-degree thinking we employ” said Susan Chodakewitz, President and CEO of Nathan Associates. “Nathan Associates’ broad experience and expertise is a force multiplier, and we’re justifiably proud of our unique ability to forecast a client’s needs and integrate them into our services.”

Led by Senior Vice President and Chief Growth Officer Dr. Eileen Parise, Federal Services helps federal agencies design solutions to preempt tomorrow’s problems.

Just as in International Development offerings, Federal Services’ work will be about more than merely business. From enacting substantive change to answering real issues at every level, the new business line is committed to bringing the same humanitarian sensibility to its work with new federal actors.

“Nathan Associates is poised to help federal agencies establish a tailored and integrated approach to their respective missions and challenges. We are a multi-purpose company that taps into its 75 years of experience to provide successful programs with a greater impact. We don’t recreate the wheel because this is our wheelhouse–integrating greater depth to agencies’ respective missions while adapting to current domestic and global world realities.” said Dr. Parise.

Nathan Associates has helped policymakers, private sector partners, and stakeholders make informed decisions by basing program implementation on objective economic principles and international best practices. From broader macroeconomic policy analyses to public administration and estimating impacts of proposed policies, Federal Services offers federal agencies technically rigorous yet practical solutions to tackle their most pressing financial, economic and program needs. No other consulting firm has the deep bench of in-house expertise and knowledge to rapidly respond to clients’ changing needs,

Learn more about Federal Services’ offerings: www.nathaninc.com/federal-services. For more on Nathan Associates, visit our website: www.nathaninc.com

Federal reserves or central banks in any country focus on three major mandates: maintaining stable prices, maximizing employment, and moderating long run interest rates. But in practical terms, they work on controlling inflation to maintain stable prices and low long run borrowing costs.

Balancing these mandates is a challenge, as growth often stimulates higher prices and more countries have increasingly added employment or economic growth mandates to central bank objectives—including some in Nathan Associates’ portfolio for instance as Papua New Guinea added a non-resource growth mandate in 2020.

This works well in normal and more stable times, but with the growing economic instability, supply chain disruptions, the cost-of-living crisis, and as policymakers seek answers to reign in prices without hurting growth, the obvious question becomes: how aggressively will central banks pursue their price mandate without undermining its maximum employment mandate? The answer will ultimately decide how—and if—inflation moderates.

Do Expectations Give a Clue?

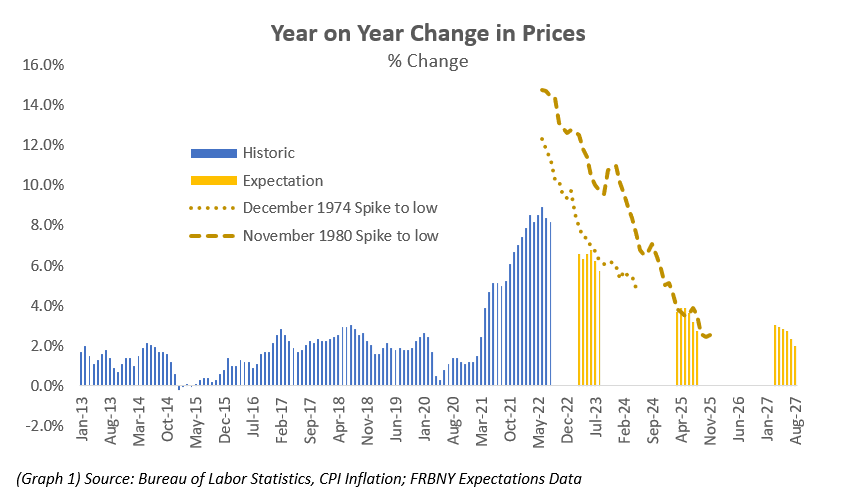

The Federal Reserve Bank of New York conducted a survey to gauge consumer expectations of inflation over a year, three years, and five years. Data on expectations provides insight into consumer views on inflation, and then potentially their likely demand for salary increases. However, it is worth noting that expectations appear to be sticky downwards—the rate of decline in expected inflation is far slower than what the Fed has achieved in inflation declines in 1974 and 1980 (Graph 1). Consumer expectations as a forecasting tool however is mostly a weak one. To better refine it, the Fed has begun looking at new methods to assess the responsiveness of inflation expectations to different economic scenarios to determine what causes people to anchor views.

Do Producer Prices Give a Clue?

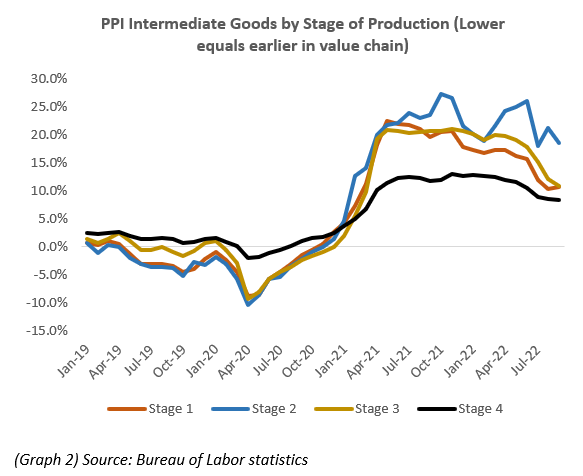

The Bureau of Labor Statistics releases data on costs of intermediate goods, which are used for the ultimate production of final demand goods—the ones us consumers buy in shops, export sell abroad, the government buys for use, or firms buy for capital. This is broken down across the stages of the value chain (see left—from early to later). Based on the trends in Graph 2, we can look at some comforting news: the earlier stage 1 firm production prices (earlier in the value chain) have moderated and even fallen off from their June 2022 peak by 2.3%. If this continues the pass through of lower costs in production could eventually mean a moderating of prices in the shops.

Can Commodity Prices and Futures Give a Clue?

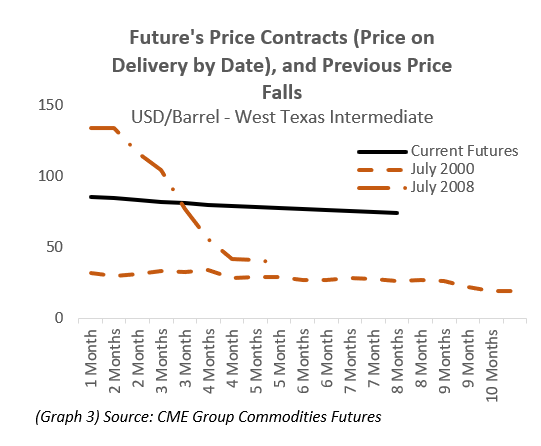

Futures prices—the price you pay now to purchase a good for delivery in the future—remain some of the better sources of data on commodities, particularly for oil and gas. They currently imply a decline of around 12% end of year 2022 to end of year 2023. This does not feed directly into consumer prices, especially given the low worldwide refining capacity. Drops in recent past have been swifter than futures prices would imply, or from a much lower base (Graph 3). Fuel and power costs make up around 4.8% of the producer price index for overall intermediate goods. and a fall in prices of 12% would mean a 0.6% direct impact on the total inflation—not insignificant when coupled with its impacts through the supply chain.

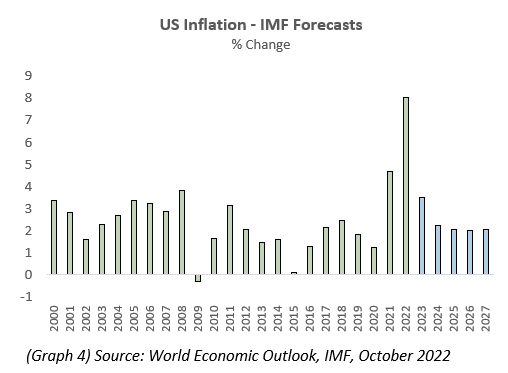

Do IMF Forecasts Give a Clue?

The International Monetary Fund is unsurprisingly bullish on the ability of the Fed to reign in prices, and the Fed’s willingness to do it regardless of the cost. The Fund anticipates the inflation in the US to drop to 3.5% next year, moderating down to the Fed target in 2024-2025. This indicates at least that the Fund believes the Fed can meet its mandate—though that in itself has opened both up for criticism for not doing enough.

So, the two biggest concerns for the Fed are likely: how quickly can they bring inflation down, and are there costs that risk it spiking back up again? And will expectations of higher inflation become part of peoples’ views of the economy?

At the moment, gratifyingly, the answer to the latter appears to be no, everyone still seems to believe in the Fed’s powers, in the former though is where the risk lies.